COVID-19 Debt Relief Measures Insufficient, Retail Borrowers Said; Fair Finance Thailand Advocates Measures for Sustainable Debt Relief

As COVID-19 epidemic still rages on in Thailand, with high levels of daily infections and death tolls, government measures to contain the epidemic such as lockdowns has led to severe disruptions of economic activities and, hence, severe drops in household incomes. Household debt which was already high before COVID-19 became a time bomb, the fuse for which becomes each household’s ability to service debt.

On 9 September 2021, Bank of Ayudhya published an article titled “COVID-19 fight – from world lessons to economic measures in Thailand.” The article cited data from Department of Business Development and Household Socio-Economic Survey to show that 754,870 businesses, or 93.9% of total, operate in 9 industries that are most affected by COVID-19 or in the most controlled areas as per government’s decree. These businesses altogether employ 24.8 million people, or 65% of the total labor force. In addition, approximately 13.7 million people or over half of this population are low-income or middle-income.

These numbers reflect people’s real lives. If the debt time bomb is not defused in time, the consequences could be deadly. Time is of the essence, because debt burden does not stay constant but rises with time and interest rates.

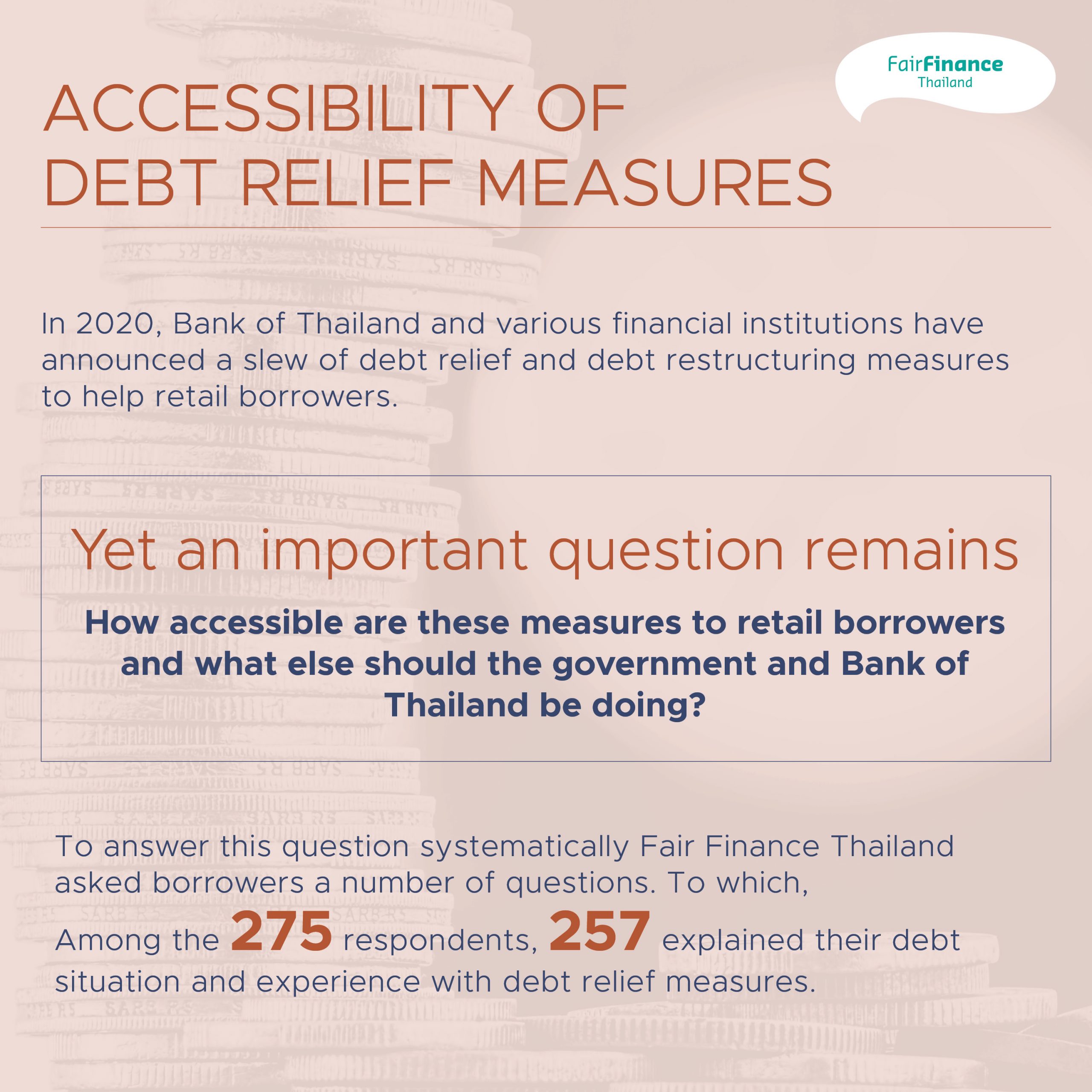

In the past year, Bank of Thailand and various financial institutions have announced a slew of debt relief and debt restructuring measures to help retail borrowers. Yet an important question that is yet to be answered systematically is: how accessible are these measures to retail borrowers, and what else should the government and Bank of Thailand be doing?

Fair Finance Thailand asked borrowers these questions directly between 23 April – 21 May 2021 by conducting an online survey. Among 275 respondents, 18 reported having no debt, the rest explained their debt situation and experience with debt relief measures.

Almost one-third income decline after the onset of COVID-19

Among 240 borrowers who disclosed their income information, it was found that its ranges from -from less than 15,000 Baht to over 100,000 Baht. Monthly income of all borrowers on an average was 116,049.5 Baht before Covid-19 was hit, but after the onset of COVID-19 average income declined by 29.7% on average, or almost one-thirds of pre-COVID-19 times.

In terms of the occupations of borrowers, those who reported being currently “unemployed” are the hardest hit, with average income declining by as much as 76%. The next worst-hit are self-employed, whose average incomes declined by 57.8%, followed by freelance, with 55.8% income decline on average. COVID-19 negatively affects people across all occupations, although some occupations are less affected compared to others: government workers and employees of state-owned enterprise reported only 3.7% income decline on average, while office workers saw their incomes declined by 15.6% on average.

Debt burden rose across the board, with insufficient income to service debt

Among 244 borrowers who disclose debt characteristics, 68.9% reported having borrowed from 1-3 creditors, while the rest borrowed from 4 or more sources. There are 4% of borrowers who reported having more than 8 creditors.

In addition to borrowing from different sources, borrowers also incurred different types of debt. Creditors reported in this survey can be grouped into three categories: private banks and state-owned specialized financial institutions (SFIs), non-financial institutions, and informal debt. In terms of debt types, information from 221 borrowers totaling 551 agreements saw that the majority, 29.6%, are credit card debt, 23.4% are personal loans, 21.1% are housing loans, and 11.3% are cash cards.

Information from 131 borrowers who disclose information relating to Debt Service Ratio (DSR) revealed that every occupation saw debt burden rise after the onset of COVID-19. Not surprisingly, debts rose the most for occupations that saw a precipitous decline in incomes: debt increased by 543.2% for the unemployed, 400% for farmer, and 155.8% for self-employed. In contrast, government workers whose average incomes declined the least also saw their debt increased by only 10.5%, the least compared to other occupations.

Reduce expenses or borrow other sources to repay: limited choices for debt management

Retail borrowers who responded to the survey reported a decline in income of 29.7% on average, or almost one-thirds of pre-COVID-19 income. Meanwhile, their monthly Debt Service Ratio increased from 56.9% on average to 147.8% on average.

Faced with this dilemma, most borrowers resorted mainly to two measures: 1) attempt to reduce household expenses, and 2) borrow from other sources to repay.

Survey results found that most borrowers tried not to incur more debt unless necessary: 64% of borrowers tried to reduce expenses, 37% participated in debt relief measures offered by creditors, and 35.8% tried to find alternative sources of income. In terms of borrowing more to service existing debt, 24.1% of borrowers borrowed more from financial institutions, 18.7% borrowed interest-free from acquaintances, and 10% borrowed from informal lenders.

Among those who borrowed more from informal lenders, 40% are daily wage earners, 28.6% are farmers, and 12.5% are the unemployed. These occupations face extreme income uncertainties, have little or no savings, and have trouble accessing quick credit from formal financial institutions.

Some borrowers decided not to join debt relief programs; some were rejected

Bank of Thailand (BOT) has announced various debt relief programs in coordination with financial institutions. Still, among 165 borrowers who disclosed information, more than half or 92 borrowers said they did not join any debt relief program. 44 borrowers reported joining debt relief programs of every credit from which they borrow, and 29 borrowers said they only joined the program involving several creditors.

64 borrowers disclosed that they decided not to join any debt relief program, 57 borrowers said their situation does not qualify them for the program, and 15 borrowers said they have applied to join, but their applications were rejected.

Those 64 borrowers who decided not to join the program cited three most common reasons: 73.4% do not want a higher debt burden post-measure, 31.3% saw the programs as providing only temporary relief, and 21.9% said applying to the program was too cumbersome and takes too long.

Of the 15 borrowers whose application to join were rejected by creditors, 40% said that creditors informed that they did not qualify, and 26.7% said they were rejected without receiving any reason from creditors.

5 recommendations from borrowers, and 6 recommendations from Fair Finance Thailand for “new life” of borrowers post-COVID-19

All 257 borrowers who participated in the survey had various recommendations on addition measures that they need. Their suggestions can be grouped into 5 recommendations as follows

1. Lengthen debt relief period 21.0%

2. Reduce interest rate 15.6%

3. Income relief payment from the government 9.7%

4. More flexible debt repayment schedule 5.8%

5. Low-interest loans 2.3%

In addition, many borrowers expected the government to help negotiate with creditors and pass more direct aid measures. They also expect Bank of Thailand to encourage borrowers in good standing to be able to refinance debt at low interest rate, before their debt becomes non-performing loans (NPL). Borrowers also expect practical debt restructuring programs for those that have become NPLs, including appropriate changes in interest rates and debt installment amounts, to enable borrowers to repay during COVID-19 crisis.

Fair Finance Thailand proposes 6 policy recommendations to the Bank of Thailand and the government. The coalition believes these recommendations are necessary in creating a sustainable path out of household debt crisis.

1. Bank of Thailand should conduct regular survey of borrowers, in order to improve debt relief programs and eliminate obstacles that hamper their access to the programs.

2. Government should provide direct and sufficient remedies to help alleviate income shortfalls, i.e. income relief payment.

3. Bank of Thailand should consider abolishing all mandatory interest rate ceilings, to spur innovation and competition in the market. The regulator’s attention should be shifted toward effective enforcement of market conduct regulations, to ensure a free and fair level playing field.

4. Bank of Thailand should set up Alternative Dispute Resolution (ADRs) to facilitate fair and orderly dispute resolutions between borrowers and creditors.

5. Thailand’s Bankruptcy Act should be amended to allow voluntary bankruptcy proceedings for individual borrowers (currently the voluntary bankruptcy proceedings are only available to juristic persons).

6. To increase financial inclusion, in the short term Specialized Financial Institutions (SFIs) should consider short-term credit for low-income borrowers. In the long run, National Collateral Registry (NCR) should be set up and secured with Blockchain technology.

For more information, see the COVID-19 household debt case study on Fair Finance Thailand website: https://fairfinancethailand.org/bank-guide/case-studies/covid-19-debt-case-study/